“An investment in knowledge pays the best interest.” –Benjamin Franklin

Taking Advantage of Tax Shelters

Introduction | What is a Tax Shelter?

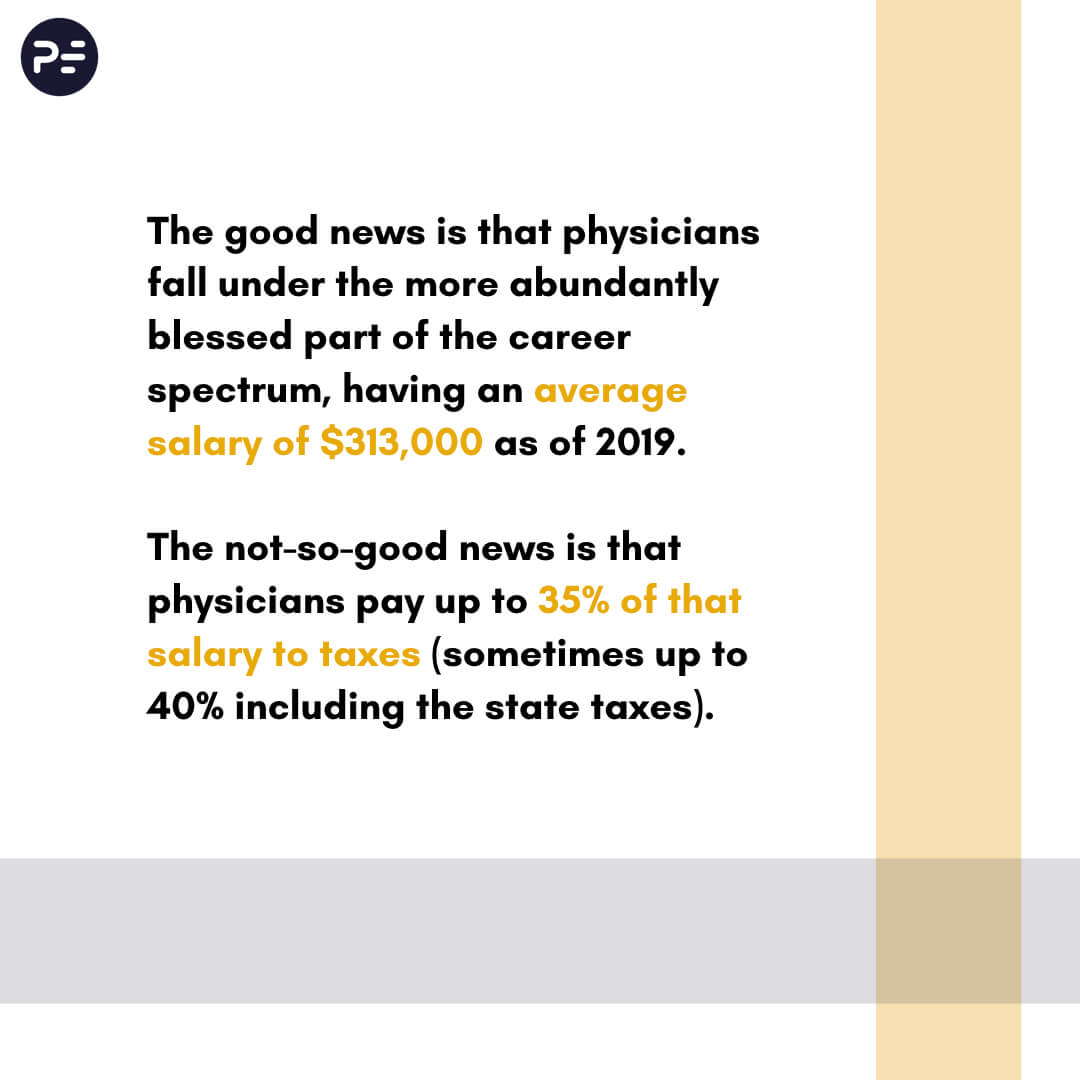

Tax Shelters for High W-2 Income | Every Doctor Must Read This! We have good news and not-so-good news. The good news is that physicians fall under the more abundantly blessed part of the career spectrum, having an average salary of $313,000 as of 2019. The not-so-good news is that physicians like you pay up to 35% of that salary to taxes (sometimes up to 40% including the state taxes). The thing is, no matter what investment or profession you are a player in, tax is an inevitable aspect of any financial landscape. It’s something you should embrace, and not escape or dread, especially since there are a number of tax shelter strategies you can use to minimize tax liabilities.

If you’re wondering, “What is a tax shelter and how can it benefit me as a physician”, there are a lot of ways to go about this question. By definition, tax shelters are methods which help you reduce your tax bill. Before we dive into all the important reasons why tax shelter is something you should be knowledgeable about, it’s best to get this burning question out of the way – yes, tax shelters are legal.

Think of tax shelters as your financial bottom line’s best friend. It protects your wealth. It allows you to channel your hard-earned money into income-generating assets such as real estate syndications, apartment complex buying, and other profitable streams of income. Take note that your high W-2 income is also a financial strength which makes you eligible to be an accredited investor. Every dollar you save from liabilities like expenses and taxes is another dollar added to your investment capital. This will put you in the right path for wealth generation and financial freedom.

These are just some of the reasons why it’s a huge advantage to know the answers to the question, “What is a tax shelter?” In this blog we get into all the ways you can make the most out of the tax shelters that are available to you as a physician. Just to be clear – please know that I am not a tax advisor / CPA / financial advisor. Please consult with your tax advisor to discuss your situation.

Tax Shelters for Physicians in the US

1. Real Estate Professional Status (REPS)

Did you know that by simply declaring yourself (or your spouse) a realtor by profession, you are already eligible to deduct your real estate losses from your taxable income? By definition, Real Estate Professional Status, or what they refer to as REPS, is a tax-status within the IRS. You don’t need to undergo training or have a license to qualify as a real estate professional.

In order to declare your Real Estate Professional Status, you simply need to meet the following primary qualifications:

- Your material participation in real property trades and businesses should account for at least 50% of all the personal services you rendered throughout a year.

- You must have spent a minimum of 750 hours in actual trade and business involving your material participation.

In any case most of your time is devoted to clinical services, you may have your spouse (non-working or part-time working) declare themselves as the real estate professional. Take note that your taxes must be filed jointly in order to make this strategy work. I personally know of many physician colleagues that haven’t paid a single dollar in taxes, by utilizing the REPS and passive paper losses from real estate investment, to help offset their high W-2 income. For a more comprehensive guide on declaring your Real Estate Professional Status, read our other blog here.

2. Oil and Gas Investment Partnerships

For extra wealthy, seasoned investors, oil and gas investments tax deductions stand out as a vehicle that is great at growing wealth. Increased interest on domestic energy production here in the US has paved the way for numerous tax shelters and investment opportunities, and oil is definitely part of the lucky roster. There are many methods to get into oil and gas investments – mutual funds, partnerships, royalties, and working benefits. For the purpose of getting the best possible tax shelter outcome, the partnership method reaps the most oil and gas investment tax deductions, which we will discuss in a bit. Nevertheless, it’s important to study all methods to see which works best for you. To learn more about the different oil and gas investment methods, you can refer here.

Moving on to the tax benefits of oil and gas investing, there are different variations available which are found nowhere else on the tax code. What’s awesome about the tax benefits of oil and gas investing is that the limits are few to none, except for the small producer limit. This means that even wealthy physician investors can directly invest in oil and gas partnerships, as long as they limit their ownership to 1,000 barrels of oil per day. Considering the current market turbulence, investments in Oil and Gas are extremely risky in my opinion. Hence it is very important to collaborate with experience Oil and Gas operators/syndicators that have a proven track record of successful outcomes. Without further ado, the tax benefits of oil and gas investing include:

- Intangible Drilling Costs

- This includes everything but the actual drilling equipment – labor, chemicals, mud, grease, and other miscellaneous items needed for drilling which are considered intangible. These costs usually comprise about 65-80% of the total cost spent for oil drilling and are 100% tax deductible within the same year the expenses are incurred. Another major perk: this is considered a gold mine in oil and gas investments tax deductions because it doesn’t even matter if the chosen area to be drilled will actually produce or strike oil – the incurred costs will still remain eligible for tax shelter.

- Tangible Drilling Costs

- This pertains to the actual expenses incurred for the drilling equipment. The following costs are 100% deductible and are also considered as major tax benefits of oil and gas investing, but remember that tangible costs must report depreciation over seven years.

- Active vs. Passive Income

- In the tax code, a working interest (not a royalty interest) in an oil and gas investment is not considered passive income. This implies that all net losses are considered active income incurred, which coincides with well-head production. The aforementioned can be offset against other streams of income, including wages, interest, and capital gains.

- Small Producer Tax Exemptions

- This may be one of the most advantageous tax benefits of oil and gas investing. Popularly known as the “depletion allowance”, this form of oil and gas investments tax deductions excludes 15% from the total gross income incurred. You are eligible for this tax exemption for as long as your investment is able to produce or refine less than 50,000 oil barrels per day. Investments which include more than 1,000 oil barrels per day, or 6 million cubic feet of gas per day, are excluded.

- Lease Costs

- This includes the acquisition of lease and mineral rights, lease operating costs, and all pertinent administrative, legal, and accounting costs incurred. The following incurred expenses should be capitalized and deducted over the period of the lease through your depletion allowance.

- Alternative Minimum Tax

- Any excess intangible drilling costs incurred are also part of oil and gas investment tax deductions. This is considered a “preference item” on the Alternative Minimum Tax (AMT) Return. This was established to ensure that tax payers would pay a minimum amount of taxes by recalculating the income tax they owe, adding back the “preferred item” or tax deduction.

- Tax Shelter for Marginal Wells

- As a way to protect remaining marginal wells, the House of Representatives and the US Senate passed a bill granting tax credits of up to $9 per day, per well unit, for marginal oil and natural gas wells. Commonly known as stripper wells, marginal wells pump approximately 90,000 cubic feet of natural gas or 15 barrels of crude oil per day. These wells account for a maximum of 10% of gas and 25% of crude oil produced in the US, respectively.

- Enhanced Recovery Credit

- Over time, it becomes increasingly hard and costly to extract oil from an area because pressure from within the well decreases. Even though production declines, there is almost always oil to be extracted and this is why the government encourages different methods of extraction.

- If it so happens you owe an operational mineral interest and have qualified operational expenses due to enhanced recovery efforts, the government entitles you to a 15% credit within the same year the costs were incurred.

3. Conservation Land Easements

A word of warning: there is much controversy attached to this next tax shelter method, which is why it’s best to proceed with caution. A conservation land easement, also referred to as a conservation agreement, is a voluntary and legally binding agreement between a land owner and a land trust or government agency.

When a landowner decides to donate an easement to a land trust or government agency, they are giving away a portion of rights affiliated with the land. This is usually done under the premise that the piece of land holds intrinsic value – it could be a migration field for rare species, a green space amidst a highly developed area, or it could be congruent with a valuable body of nature such as a river or a forest. Often perceived as a “charitable donation”, these donated properties entitle you to conservation easements tax benefits depending on how much value the property is appraised.

Before you get into this tax shelter method, it is crucial to know that the federal government keeps a wary eye on such tax strategies. Not to discourage you or anything but many investors and millionaires have been apprehended for “abusing” this tax scheme by declaring bogus deductions.

According to ProPublica, there is nothing wrong with conservation easement tax benefits in its purest form. “In its original, legitimate form, [a conservation land easement] is granted when a landowner permanently protects pristine land from development. In that scenario, the public enjoys the benefit of undeveloped land and the taxpayer gets a charitable deduction. By contrast, the syndicated form, created and packaged by profit-seeking middlemen known as “promoters,” involves buying up land, finding an appraiser willing to declare that it has huge development value and thus is worth many times the purchase price, then selling stakes in the deal to wealthy investors who extract tax deductions that are often five or more times what they put in.”

We emphasize: although it may be a rather sensitive tax shelter undertaking, conservation easement tax benefits are legal and highly advantageous as long as done properly. Tom Wheelwright, a CPA and CEO of WealthAbility, expresses, “Owners of undeveloped land who don’t know what to do with it can get a charitable deduction for putting a conservation easement on the property. The IRS will always scrutinize it, but if it’s done correctly, it’s a great opportunity for wealthy clients that don’t know what to do with the land.”

4. Other Strategies

Whether big or small, any method that contributes to positive tax shelter scenarios are worth considering. These are other strategies you can utilize to save money from taxes:

- Invest in Municipal Bonds

- To buy a municipal bond is to lend money to a state or local entity for an agreed upon number of interest payments over a certain period of time. Once the bond has matured, the full amount of the original investment is returned to the buyer.

- What’s great about municipal bonds is that they are exempt from federal taxes, making it a worthwhile tax shelter strategy. These bonds may also be tax sheltered at the state and local level as well, depending on which state you reside.

- Vie for Long-Term Capital Gains

- When it comes to investments, it’s important to vie for long-term capital gains whenever possible. An added benefit for when you invest in stocks, mutual funds, bonds or real estate, long-term capital gains are attractive to investors because it provides you with a preferential tax rate of 0%, 15%, or 20%, depending on how long you’ve kept the asset under your name.

- To understand the key differences between long-term and short-term capital gains is crucial to developing the most favorable tax shelter outcome. Make sure to consult a trusted CPA so that they can help you determine when and how to sell your assets to offset losses and maximize gains.

- Begin a Business

- Apart from your primary job as a physician, side hustles offer a lot of advantageous tax shelter strategies. There are many business expenses which can be deducted from your income tax bill, such as health insurance premiums. As per IRS guidelines, a business owner can deduct a portion of their home expenses with the home office deduction. Some utility costs which are used in the business are also a tried and tested form of tax shelter.

- Alternatively, creating a structure is also a tax shelter strategy you can maximize. Limited liability (LLC) companies are usually created to manage multiple investments. This could include portfolio assets, real estate, or a business.

- Maximize Tax Sheltered Annuity

- Similar to a 401(k) plan, a tax sheltered annuity plan is a retirement plan offered by public schools and charities. Also referred to as the 403(b) plan, a tax sheltered annuity plan allows employees to defer a portion of their salaries into individual accounts.

- For 2020, you are now able to reduce $19,500 if you contribute to a 401(k) plan or a 403(b) plan. Those who are 50 years old and above can add $6,000 to their basic workplace retirement plan. Even those who don’t have a retirement plan at work can get a tax shelter if they contribute up to $6,000 ($7,000 for those who are 50 years old and above) to a traditional individual retirement account (IRA).

- The SECURE Act covers all newly implemented legislations on tax shelters that affect your retirement planning and tax shelter strategies, such as the removal of age limit for contributions to a traditional IRA. For a more comprehensive discussion on the terms and inclusions of the SECURE Act, click here.

- Create a Health Savings Account (HSA)

- Did you know that a health savings account from a high-deductible health insurance plan can also provide you with a favorable tax shelter scenario? Much like a 401(k) plan, money is turned over to a HSA before taxes. As of 2020, the maximum contribution is $3,550 for an individual and $7,100 for families. This means that your money grows without you having to pay taxes on your earnings.

- Acquire IRS Credits

- You’ll be surprised to know that there are actually many IRS tax credits which you can take advantage of. A perfect example is the Earned Income Tax Credit. As of 2019, a low-income tax payer may be able to receive up to $529 in credits. Taxpayers with three or more children may be eligible for up to $6,557 in credits.

- On the other hand, if you are a student, the American Opportunity Tax Credit provides up to $2,500 per year for students who are eligible. For moderate and lower-income individuals, the Saver’s Credit is perfect for those who are trying to save up for retirement. These individuals can receive credit of up to half of their contributions to a retirement plan or an IRA. Lastly, the Child and Dependent Care Credit can offset up to $6,000 worth of credit in relation to the expenses of raising kids, depending on a person’s income.

- Increase Equity Exposure and Manage Gains

- It’s always best to explore avenues where you can get a bigger piece of the money-making pie. If you haven’t yet, try investing in stocks to increase your equity exposure. Multiple streams of income will allow you to soften the blow of any losses you may incur and manage your gains responsibly.

- It’s also important to note that some investments bless you with better tax shelter scenarios when you hold on to them longer. Case in point, when it comes to investing in stocks, taxes are typically lower than the tax rate you would get on wage income if the stock units were held for more than a year.

- Tax shelters are also generous when it comes to long-term capital gains. Federal tax brackets are anywhere from 10% for the lowest earner to 37% for the highest. Short-term capital gains taxes from stocks which were held for less than a year are based on your federal tax bracket.

- For more information on 2020 Federal Tax Brackets and Tax Rates on Capital Gains and Dividends, click here.

- Capitalize on Real Estate and Capital Exemptions

- As you already know, real estate and capital investments are great tax shelter strategies. These methods offer unbelievably profitable tax benefits. Thanks to the recently updated tax law, tax shelters have now doubly improved. Individuals are now able to claim up to $11.18 million in comparison to the $5.29 million limit per person in 2017. This tax exemption expires after 2025 is over so it’s best to take advantage while it still applies.

- 1031 Exchanges

- A 1031 Exchange is one of many ways you can take advantage of all the tax benefits real estate can offer. This form of tax shelter allows you to defer taxes on your capital gains (take note: defer, not eliminate). You can make this happen by furnishing a report to be submitted to the IRS stating that the money (or at least a portion of it) to be used for buying a property came from selling another property. This ‘like-kind exchange’ is completely legal and exists under Section 1031 of the IRS Code. For a comprehensive guide on filing 1031 exchanges, you can refer to this blog.

Summary | Tax Shelters for Physicians

If you have reached this far, you may be overwhelmed with all this information. Don’t worry, it really takes time to study all the tax shelters made available to you. Here’s a pro tip: a simple way to organize all your taxes is to categorize them into three: taxable, tax-deferred (those which can be lowered or settled at a later date), and tax-free. Be patient with all the intensive research that needs to be done and don’t hesitate to seek help when needed. A trusted CPA in your corner will definitely help create the best scenarios of tax shelters out of your existing investment portfolio. Try to interview several tax advisors / CPAs to find a perfect fit for you. There is a ton of variation in the services offered by these CPA firms, so please be careful to select the one that offers you a customized solution. By maximizing all these legally accredited tax shelter strategies, you are able to protect and grow your wealth and maximize your high W-2 income as a physician.

Here at PhysicianEstate, we welcome all physician entrepreneurs to learn about commercial real estate investments, rental property investments, and wealth generation. We encourage all physicians to eventually become real estate physician investors. We know a great deal about Who – What – Why – How.

Stay in touch with us by signing up for our newsletter. The newsletter will keep you up to speed on the current real estate investments we are looking at, provide physicians with investment opportunities, and much more.

Legal Disclaimer: This is not investment advice. I am not a legal and/or investment advisor. This is my personal blog, and all information found here, including any ideas, opinions, views, predictions, forecasts, commentaries, suggestions, or stock picks, expressed or implied herein, are for informational, entertainment or educational purposes only and should not be construed as personal investment advice. These are my views, it is not a production of my employer, nor is it affiliated with any broker/dealer or registered investment advisor. While the information provided is believed to be accurate, it may include errors or inaccuracies. To the maximum extent permitted by law, PhysicianEstate disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations prove to be inaccurate, incomplete or unreliable, or result in any investment or other losses. You should consult with an attorney or other professional to determine what may be best for your individual needs. Your use of the information on the website or materials linked from the Web is at your own risk.