How Physicians Can Shelter W-2 Income with Real Estate Professional Status (REPS)

How Can Physicians Shelter W-2 Income with Real Estate Professional Status (REPS)?

You probably heard about how real estate investment can have tax benefits. We have written two comprehensive blog posts about real estate tax benefits for physician investors. You can read these blog posts here and here.

The average salary of physicians in the US stood at $313,000 in 2019.

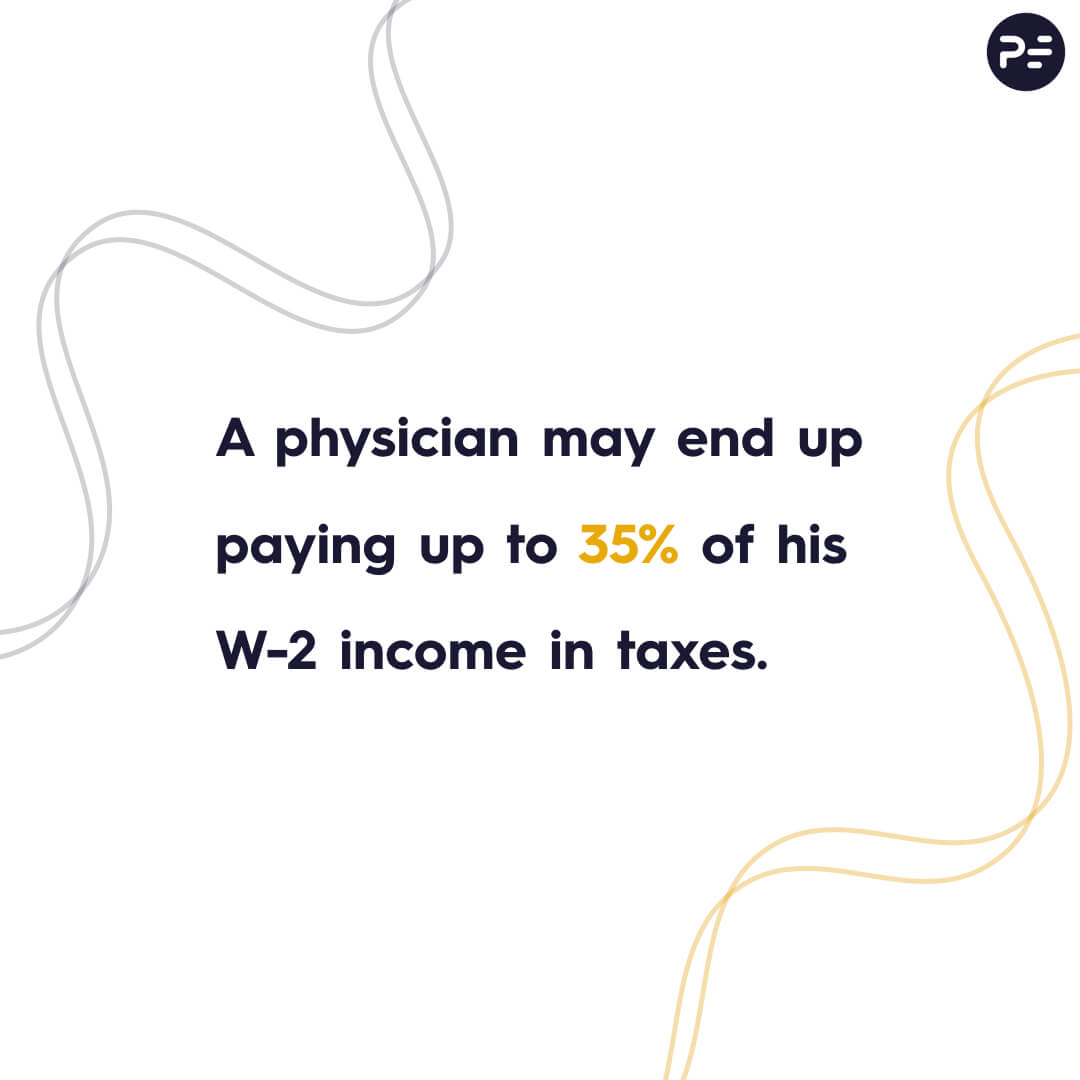

As impressive as it may sound, a significant portion of this income goes into taxes. In fact, a physician may end up paying up to 35% of his W-2 income in taxes.

However, did you know that some physicians (a very low percentage) are lowering their tax bills through Real Estate Professional Status (REPS)?

A survey indicates that as many as 8% of physicians are either using REP status to cut their taxable income or planning to use it in the near future.

Would you like to know more about this tax-saving strategy for physicians? This post will focus on REPS, how you can qualify for it, and the advantages as well as limitations of this strategy.

Learn how you can reduce tax bill by using cost segregation and bonus depreciation on this blog post.

What is Real Estate Professional Status?

The Definition | Real Estate Professional Status

Real Estate Professional Status is essentially a tax-status within the IRS. It doesn’t require you to become a realtor or leave your profession to become an active realtor. The IRS allows real estate professionals to deduct their losses from their taxable income.

You don’t need a license or training to qualify as a real estate professional.

How Can You Qualify for Real Estate Professional Status (REPS)?

There are two primary qualifications for real estate professional status.

- Your material participation in real property trades and businesses should account for at least 50% of all the personal services you rendered throughout a year.

- You spend over 750 hours in actual trade and businesses involving your material participation.

In short, you need to declare real estate as your primary profession. For physicians devoting most of their time to clinical services, it is possible to have your spouse (non-working or part-time working) qualify for real estate professional status. One must note that you will have to file taxes jointly in order to make this entire strategy work.

Your spouse should spend at least 750 hours managing the business through meaningful material participation. The trick here is to understand how the IRS defines material participation. As long as your spouse actively partakes in any development, management, and operational aspect of real estate you own, he or she can qualify for REPS.

Key takeaways of 750-hours rule – REPS:

- Since your spouse is non-working or working part-time only, he or she already meets the qualification of having real estate as her primary business activity.

- The second one is material participation. Your spouse needs to be involved in the day-to-day operational activities in addition to merely managing the property or getting status updates from your property manager. Ideally, your spouse would want to be involved in any repair, construction, or renovation projects. It could be overseeing the entire project or coordinating with the contractors/property managers or even getting supplies.

- A critical part of this 750-hours rule is to have sufficient documentation to indicate how you spent these hours. It could be using something as simple as Google spreadsheets or using a separate email account to track all the communication with contractors, managers, etc.

- Out of these 750-hours, your spouse must spend at least 500 hours on real estate that you own. The remaining 250 hours can be spent on additional management or related activities. Your spouse should also hold at least a 5% stake in these properties to satisfy material participation rules.

- If you own more than one property, you can combine all of these activities under a single rental real estate activity, as mentioned under Sec. 469(c)(7)(A) of the IRC. As a practical tip, you may want to start with a multi-family apartment or have at least a couple of units in your portfolio to justify active participation of 750 hours or more.

Material participation: Here is a resource indicating seven quantitative tests for material participation.

How It Can Help Physicians Lower Taxes on W-2 Income

Once you or spouse becomes a real estate professional, you can deduct any losses incurred within rental properties from your W-2 income.

The beauty of the IRS is that it allows you to claim a wide variety of deductions for rental properties. Some of these deductions include depreciation, repair or maintenance expenses, insurance, and any expenses incurred for necessary supplies.

As a real estate professional, you can enjoy the benefits of cost segregation and take a massive income tax benefit through “phantom expenses.”

How Do You Get a Real Estate Professional Status?

A Step-by-Step Guide to a Real Estate Professional Status

If you’re seeking savings through taxes for real estate using the REPS status, here is a step-by-step guide to doing it.

Step 1: Create a plan to qualify for real estate professional status.

Since you already understand the qualifications for a real estate professional status, start by deciding which of the two spouses will apply for REPS.

Some important things to consider:

- For both working spouses, one has to cut on their current occupation (medical or any other) and give more time to real estate.

- In the case of a non-working spouse applying for REPS, it is essential to give up to 750 hours every year to your real estate business.

- It is critical to have material participation in your real estate portfolio. Make sure to seek expert help to go through the litmus test for REPS qualification (7 quantitative tests).

Step 2: Seek legal help to set up the structure for your real estate portfolio.

Real estate professional status helps you realize real estate losses as active-income losses, making it critical to have the right legal structure and documentation in place. Ideally, you would want to work with a CPA/tax attorney having relevant experience.

Step 3: Work on your finances to invest in real estate, especially during the early stage.

A critical part of the entire strategy is to have sizable finances to purchase real estate, especially during the early stage. We briefly discussed how having multiple units would make it easy to satisfy the 750-hours minimum participation.

Step 4: Be a diligent record keeper of all your real estate activities.

As a real estate professional, you need to be ready to face audits at any time. The trick is to be as diligent as possible with your records and documentation as you can. You can start by using a separate email account for all your communication, maintain a digital copy of bills or a folder for hard copies, and accounting software to track your expenses as well as income from the property.

What Are the Advantages of the REPS Strategy for Medical Professionals?

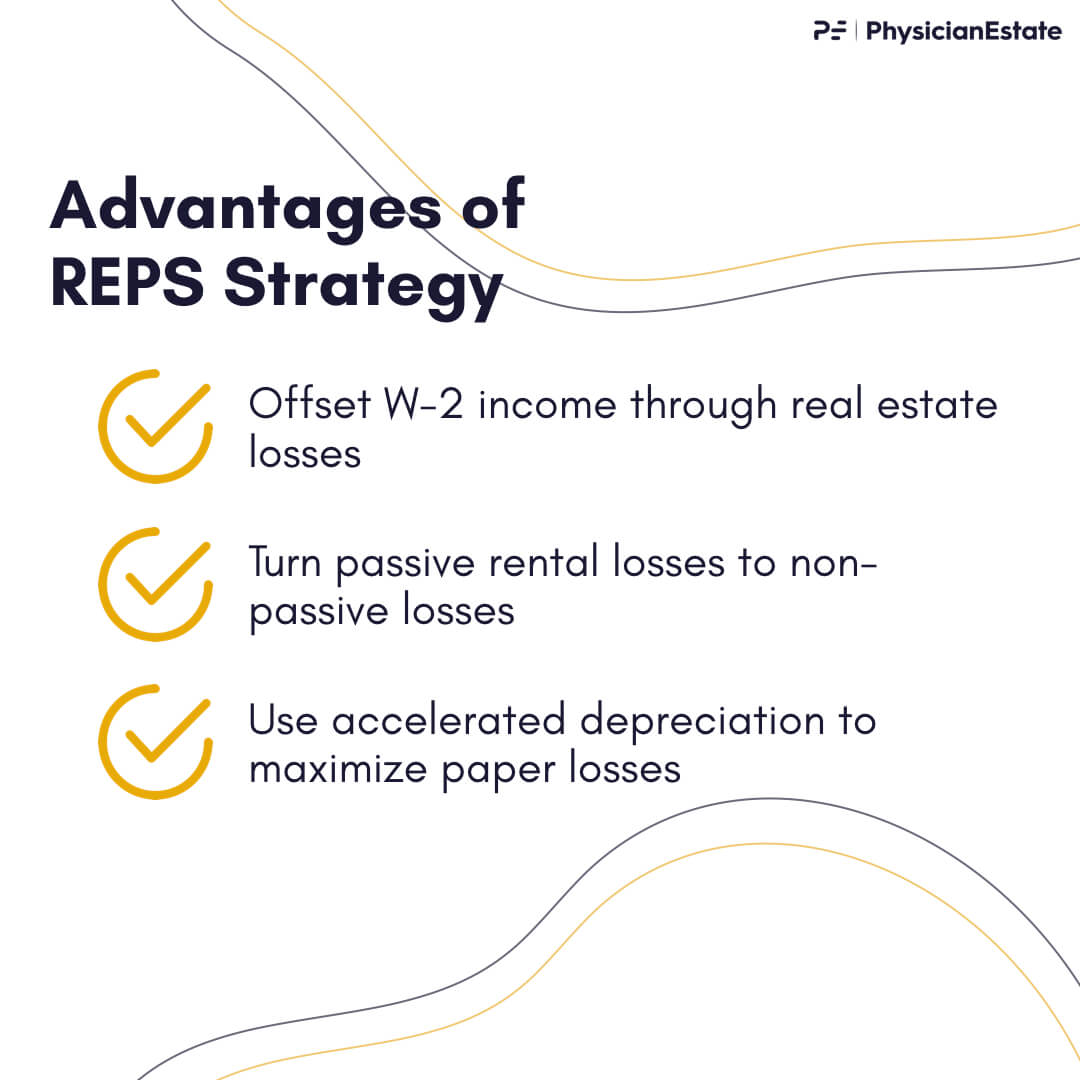

- Offset W-2 income through real estate losses: One of the primary benefits of the real estate professional status for physicians is the ability to offset your real estate losses from W-2 income. Traditionally, individuals with salaries above $150,000 miss out on these benefits, but real estate professional status allows medical professionals to offset their income irrespective of their salary.

-

- Example: If you are a physician making $400,000 annual income from your W-2 job, you probably take home only $250,000; and end up paying $150,000 in taxes. If you plan and execute the REP status effectively, you can divert your passive losses in real estate to shelter your W-2 income from being taxed. For instance, if you buy a $1,500,000 multifamily apartment that needs minor renovations, you cost segregated – accelerated depreciation for the first year may be up to $300,000. This means, you incurred passive losses of about $300,000 from your real estate. If you qualify for REPS, you are able to use this $300,000 passive loss in real estate to shelter your W-2 salary. Now, instead of paying taxes on $400,000 W-2 income (~$150,000), you only have to pay taxes on $100,000 of your W-2 income (~20,000). You see, that right there is an extremely lucrative tax strategy.

- In the above example, if you made $400,000 annual W-2 income, you pay $150,000 in taxes without REPS. With REPS, you only pay $20,000 in taxes. With REPS, you are taking home an additional $130,000.

- Turn passive rental losses to non-passive losses: As per the IRS, individual investors earning beyond $150,000 can use passive losses to offset their passive income in the future, giving little instant relief. Real estate professional status allows medical professionals to turn their passive rental losses into non-passive losses, thereby allowing deductions from their active income (W-2 or 1099 income).

- Use accelerated depreciation to maximize paper losses: For those trying to boost deductions through taxes in real estate, the IRS allows paper deductions, called depreciation. As a real estate professional, you can maximize your deductions through accelerated depreciation or cost segregation. These strategies will enable you to claim all of your deductions upfront instead of claiming annual depreciation annually.

Are There Any Limitations to the REPS Strategy?

- Have to make real estate your primary profession: First, you need to take up real estate as your primary profession, putting more than half of your working hours towards real estate activities, ensuring material participation. It isn’t a feasible solution for working couples or single professionals.

- Your spouse must be willing to put in the work: Your spouse will have to put in an enormous amount of work, at least 750 hours, to qualify as a real estate professional. Make sure that your spouse has sufficient flexibility to fulfill this additional duty.

- You can realize significant benefits only with a sizable real estate portfolio: In order to book considerable benefits, you’ll need a big enough real estate portfolio. One must note that qualifying the 750-hours rules becomes more comfortable with multiple properties.

- You have to follow strict rules and be diligent in your documentation: Not only will you be required to track your time distribution, but you’ll need detailed notes to justify how you used it for your business. The IRS is strict when it comes to documentation, so you’ll add more responsibilities as you become a real estate professional.

Bottomline

Becoming a real estate professional could mean significant gains for you as a medical professional, especially as a means to hedge your W-2 income. It will require some extra efforts and walking on a thin legal line, but the monetary benefits are worth the work.

Are you a real estate professional or trying to claim the status? Kindly share your experiences in the comments section below.

Here at PhysicianEstate, we welcome all physician entrepreneurs to learn about commercial real estate investments, rental property investments, and wealth generation. We encourage all physicians to eventually become real estate physician investors. We know a great deal about Who – What – Why – How.

Stay in touch with us by signing up for our newsletter. The newsletter will keep you up to speed on the current real estate investments we are looking at, provide physicians with investment opportunities, and much more.

Legal Disclaimer: This is not investment advice. I am not a legal and/or investment advisor. This is my personal blog, and all information found here, including any ideas, opinions, views, predictions, forecasts, commentaries, suggestions, or stock picks, expressed or implied herein, are for informational, entertainment or educational purposes only and should not be construed as personal investment advice. These are my views, it is not a production of my employer, nor is it affiliated with any broker/dealer or registered investment advisor. While the information provided is believed to be accurate, it may include errors or inaccuracies. To the maximum extent permitted by law, PhysicianEstate disclaims any and all liability in the event any information, commentary, analysis, opinions, advice and/or recommendations prove to be inaccurate, incomplete or unreliable, or result in any investment or other losses. You should consult with an attorney or other professional to determine what may be best for your individual needs. Your use of the information on the website or materials linked from the Web is at your own risk.